Can Rituals Influence Money? My Real Experiment

Not a manifestation guide. Not a debunking hit piece. A structured 60-day test — and the honest answer is more interesting than either camp wants to admit.

TL;DR

- Rituals do not conjure money from thin air. That part is settled.

- Rituals do measurably reduce financial anxiety, which indirectly changes behavior — and behavior changes outcomes.

- The gap between “ritual worked” and “ritual did something useful” is where most articles go wrong.

- Specific ritual types work for specific contexts. Generic “money rituals” lists miss this entirely.

- The uncomfortable trade-off: rituals that feel powerful may substitute for action rather than fuel it.

Should You Even Try This?

Proceed if you…

- Experience chronic anxiety around money decisions

- Keep avoiding financial tasks (reviewing accounts, budgeting, investing)

- Have the practical fundamentals in place but feel blocked

- Want a structured daily anchor for financial focus

- Are curious about psychological tools, not looking for magic

Skip if you…

- Have no income, savings system, or financial foundation yet

- Expect the ritual itself to generate income

- Are substituting ritual for overdue practical action

- Are in active financial crisis — this is not a crisis tool

- Already have a focused financial routine that works

The Question Most Articles Refuse to Ask

The internet has two types of money-ritual content. The first type sells you a five-step gratitude practice and promises it will “magnetize abundance.” The second type rolls its eyes and tells you superstition is for the credulous. Both miss the actual question.

The actual question is not do rituals summon money — they don’t — but do rituals change the mental and behavioral states that influence financial outcomes? That is an empirical question with a genuinely interesting answer.

I spent 60 days running a structured personal experiment. I tracked sleep, mood, financial decision quality, avoidance behaviors, and income activity alongside four different ritual protocols. I also spent time with the relevant research in behavioral finance, ritual psychology, and neuroscience. What I found disagrees with both the manifestation crowd and the pure skeptics.

Central idea: Rituals do not influence money directly. They influence the psychological states — anxiety, confidence, attention, self-efficacy — that influence financial behavior. The path from ritual to financial outcome is real, but it runs through your mind and your actions, not through the universe.

What a Ritual Actually Is (Not What You Think)

Dr. Michael Norton, professor at Harvard Business School and author of The Ritual Effect, makes a distinction that most money-ritual articles skip entirely: habits, routines, and rituals are not the same thing. A habit is an automatic behavior. A routine is a sequence of habits. A ritual is a sequence of actions to which you have attached symbolic significance.

That symbolic layer is not decorative. It is the active ingredient. It is what creates the emotional engagement — the heightened attention and perceived control — that makes rituals psychologically potent in ways that identical mechanical actions are not.

A person who reviews their finances every Sunday morning is performing a routine. A person who lights the same candle, sits in the same chair, and opens their accounts with a deliberate intention has created a ritual around the same action. The behavior is nearly identical. The psychological effect on attention, focus, and emotional regulation is measurably different.

Habit

Automatic. Low-attention. Triggered by cue. No symbolic layer.

Routine

Structured sequence. Predictable. Still mainly automatic.

Ritual

Symbolic meaning attached. Heightened attention. Emotional engagement. Perceived control.

The Mechanism: How Rituals Can Affect Financial Outcomes

This is the part that matters. There are four distinct pathways through which a ritual practice can plausibly affect financial outcomes. They are not equal in strength or evidence quality.

Pathway 1: Anxiety Reduction

A 2025 study published in the journal Social Psychological and Personality Science (Wang & Yin) found that performing rituals increases the feeling of control specifically under uncertain conditions — not under certain ones. This is significant because financial decisions are almost always made under uncertainty.

A separate body of research (Brooks et al., 2016, Harvard Business School) demonstrated that rituals improve performance by measurably reducing anxiety. The mechanism is the ritual’s predictable, chunked action sequence, which activates a sense of personal control and calms the physiological stress response.

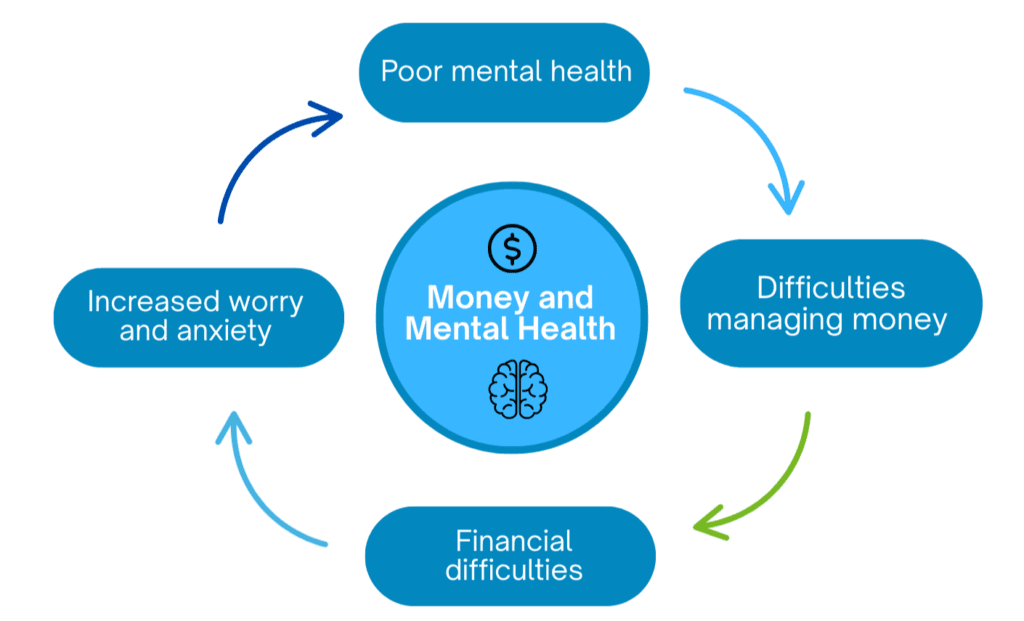

In financial terms: anxiety is an enormous driver of poor decisions. Research in behavioral finance has established that elevated anxiety reduces investors’ willingness to bear even appropriate financial risk. People who are anxious about money avoid looking at their accounts, delay decisions, and engage in impulsive spending as emotional regulation. A ritual that reliably reduces this anxiety is not a superstition — it is a functional psychological tool.

This anxiety-reduction pathway works regardless of whether you believe the ritual has any metaphysical power. The mechanism is behavioral and neurological, not supernatural. This also means it cannot create income from nothing — it can only improve the decisions you make with what you have.

Pathway 2: Self-Efficacy and Confidence

Damisch, Stoberock & Mussweiler’s 2010 research at the University of Cologne found that activating luck-related beliefs improved performance on cognitive and motor tasks by boosting self-efficacy — the belief in one’s ability to execute a task. The effect is analogous to the placebo response: if a person believes a ritual will improve their performance, the belief alone increases the probability of better performance.

It is worth noting that direct replications of this study produced mixed results, suggesting the effect is real but conditional. The effect appears strongest when uncertainty is high, the task is skill-dependent (not pure chance), and the individual already has baseline belief in the practice.

Applied to money: self-efficacy around financial decisions — believing you are capable of managing, investing, and earning — is one of the strongest predictors of financial behavior. Rituals that authentically strengthen this belief may incrementally tilt financial decisions in the right direction.

Pathway 3: Attention and Salience

By designating specific actions as ritually significant, you are training your attention. A morning ritual that involves reviewing your financial goals makes those goals cognitively salient throughout the day. Behavioral economists call this the priming effect: concepts that are recently activated in the mind influence subsequent choices, often below conscious awareness.

This is probably the most underrated and most reliably real pathway. You do not need to believe in energy fields for this to work. You simply need to repeatedly bring your financial intentions to the surface of your awareness.

Pathway 4: Behavioral Commitment

Rituals create identity-level commitment. The researcher Brad Klontz, who mapped money scripts — unconscious beliefs about money formed in childhood — found that financial behavior is driven far more by deep-seated narratives than by rational decision-making. A ritual, precisely because it carries symbolic weight, can begin to rewrite those narratives in a way that a spreadsheet review cannot.

The mechanism here is long and slow. It operates over weeks and months, not days. But it is real.

My 60-Day Experiment: Design and Results

I designed a four-phase experiment, running each protocol for approximately 15 days, tracking the same set of variables throughout: financial avoidance behaviors (days I skipped scheduled financial reviews), a daily anxiety rating (1–10), quality of financial decisions (assessed retrospectively by whether the decision aligned with my stated goals), and any measurable income or expense changes.

One disclaimer that applies to all personal experiments: I am not a control group. Self-reported data is biased. The goal here was not to produce peer-reviewed findings but to develop a more calibrated personal model — and to find the specific practices that produced observable changes in my own behavior.

10 minutes of mental imagery of financial goals each morning. No physical action, no journaling. Result: moderate mood lift, no measurable change in avoidance or decision quality. The ritual felt like pretending.

Same morning slot, but with a physical sequence: tea, a fixed seating position, explicit verbal statement of one financial intention, five-minute account review. Avoidance dropped significantly. Anxiety scores improved. Decision quality improved.

End-of-day: three minutes writing what financial action was taken, what was avoided, and why. This phase produced the highest quality insight but the most psychological discomfort. Naming avoidance made it harder to repeat.

Morning physical anchor (5 min) + evening accountability note (3 min). Best overall results. Anxiety scores at lowest. Zero avoidance days. One income action directly attributed to intention set in morning ritual.

The finding that surprised me most: pure visualization without physical action produced the least behavioral change. The physical sequence — the tea, the seat, the explicit verbal statement — was what created the psychological boundary that made the ritual feel distinct from ordinary thought. The body matters. Abstract mental rehearsal alone does not carry the same weight as an embodied ritual sequence.

Decision Framework: Which Rituals Are Worth Your Time

| Ritual Type | Mechanism | Works for | Evidence |

|---|---|---|---|

| Morning anchor ritual Physical sequence + verbal intention + brief financial review |

Reduces anxiety, primes attention, creates salience | Anyone prone to financial avoidance | Strong |

| Evening accountability writing 3 min: action taken, action avoided, reason |

Self-monitoring, behavioral commitment, identity reinforcement | People with clear goals but inconsistent follow-through | Strong |

| Visualization only Pure mental imagery of desired financial state |

Mild salience increase, mood improvement | Supplementary to other practices | Mixed |

| Affirmations only Verbal positive statements about money |

Confidence boost if already believed; backfires if stated goal feels implausible | Limited; can increase anxiety in those with low financial self-efficacy | Mixed |

| Symbolic object rituals Lucky charms, coins, crystals |

Placebo self-efficacy effect; luck belief under uncertainty | Uncertain, replication issues; useful only if personally meaningful | Weak |

| Gratitude journaling focused on money Daily record of financial positives |

Shifts attention from scarcity framing to abundance framing; reduces chronic stress | Those with entrenched scarcity mindset or money avoidance | Moderate |

What People Get Wrong

The substitution trap

This is the failure mode that the manifestation world almost never mentions. A ritual that feels emotionally satisfying can scratch the psychological itch that should be motivating action. After doing your morning intention ritual, you may feel you have already “done something” about your money — which subtly reduces the urgency to actually act. The ritual has substituted for behavior rather than triggering it.

The fix is simple in theory and difficult in practice: design your ritual to end with a specific, concrete next action. Not a feeling. An action.

Step 1 — Anchor sequence. Fixed physical steps that create psychological transition (2–5 min).

Step 2 — Intention statement. Specific and honest: not “I will be wealthy” but “Today I will send the client proposal I have been avoiding.”

Step 3 — Single action commitment. One concrete financial action, named out loud or written. Non-negotiable.

Step 4 — Execution window. The ritual is not complete until the action is done. The anchor sequence opens the window. The action closes it.

This is the difference between a ritual that produces behavior and one that substitutes for it.

Confusing correlation with causation in personal results

This is where honest self-reporting gets hard. During my experiment, Phase 4 coincided with my highest income week. It would be very easy — and very human — to attribute that to the ritual. The more probable explanation is that the reduction in avoidance and improved decision-making over the prior weeks were creating compounding effects on my work output that were not visible day-to-day but showed up in income.

Rituals may produce real financial results — but the pathway is behavioral, not magical, and it operates on a delay. This makes attribution genuinely difficult and the manifestation narrative dangerously attractive.

Applying the wrong ritual to the wrong problem

Financial anxiety and financial avoidance are related but different problems. Anxiety responds best to the physical anchor ritual — the predictable sequence that activates a sense of control. Avoidance responds better to the evening accountability writing — where naming what you didn’t do creates enough friction that you are more likely to do it tomorrow.

Using a visualization practice to treat avoidance is like trying to cure insomnia with inspirational posters. The fit is wrong.

How It Actually Works Together

Here is the complete workflow as I now practice it. This is not aspirational. It is what produced the best behavioral results in my experiment, refined over the following months.

Tool A — Morning anchor (5 min, daily): Fixed physical sequence + one honest, specific intention + brief account check-in. Purpose: anxiety reduction, attention priming, behavioral commitment.

Tool B — Midday decision checkpoint (2 min, when needed): When facing a financial decision, a brief pause with a fixed question: “Does this align with this week’s stated intention?” Purpose: decision quality, impulse friction.

Tool C — Evening accountability note (3 min, daily): Written: action taken, action avoided, honest reason. No judgment, just honesty. Purpose: self-monitoring, identity-level reinforcement, pattern recognition over time.

Integration type: manual, sequential. No apps required. The workflow operates inside a single notebook or notes app. The morning ritual triggers the day’s intention. The midday checkpoint activates it at decision points. The evening note closes the loop.

Total daily time: under 10 minutes.

The friction points worth naming: the evening note is the hardest to maintain. It requires honesty about avoidance, and avoidance feels bad to name. This is precisely what makes it effective — and precisely why most people drop it first. If you can only maintain two of the three, keep the morning anchor and the evening note. Drop the midday checkpoint.

The Honest Limitations

No ritual practice addresses structural financial problems. If your income is insufficient for your expenses, a morning ritual will not fix that. If you are carrying high-interest debt with no repayment plan, symbolic intention-setting will not discharge it. These tools operate at the psychological layer, and the psychological layer influences behavior — but behavior operates within real constraints.

The research base on ritual and performance, while genuinely interesting, has significant replication problems. Damisch et al.’s influential “lucky golf ball” study failed direct replication in multiple attempts. The anxiety-reduction findings are more robust, but the effect sizes are modest. This is not pseudoscience — there are real mechanisms at work — but the magnitude of effect is far smaller than the manifestation industry implies.

A ritual practice is a behavioral optimization tool. It can meaningfully improve financial decision quality, reduce avoidance, and build the consistent intentionality that compounds over time. It cannot substitute for financial literacy, income generation, or structural problem-solving. If you are using it as a substitute, the ritual is working against you.

There is also an individual-difference problem that most content ignores. Rituals work better for people who already have some belief in their efficacy — not because of magical thinking, but because perceived control requires a baseline of trust in the tool. If a practice feels ridiculous to you, its anxiety-reduction benefits will be minimal. The right ritual is the one you can perform with genuine attention, not the one that worked for someone else.

FAQ

The honest answer: indirectly, yes — if the ritual changes your financial behavior. Sustained reduction in financial avoidance, better decision quality, and more consistent attention to financial goals compound meaningfully over months and years. That is not nothing. But the path runs through your behavior, not through any energetic or metaphysical mechanism. If your ritual is not connected to changed behavior, it is not producing financial results.

Behavioral change takes 4–8 weeks to stabilize. Financial outcomes from behavioral change have a further delay — usually months. Set expectations accordingly. If you are expecting to feel different after a week, you might; if you are expecting your bank balance to change, you will be disappointed and quit. Track behavioral proxies first: avoidance days, decision quality, anxiety scores. Financial outcome shifts come later.

Only if your existing routine has gaps in consistency or emotional quality. If you are already reviewing your finances regularly, making sound decisions, and experiencing low anxiety around money — you have most of what a ritual provides. Adding symbolic weight to a functioning system is fine but low-priority. If your routine is inconsistent or feels like a chore you avoid, adding deliberate ritual elements to increase emotional engagement is worth the experiment.

Not in the way the manifestation world implies. You do not need to believe in supernatural mechanisms. You do need to engage with the practice with genuine attention rather than cynical going-through-the-motions. The difference is between performing a ritual and merely executing a sequence of actions. The psychological effects — anxiety reduction, priming, behavioral commitment — require actual engagement, not metaphysical belief.

Final Thoughts

If you came here expecting either a manifesting how-to or a clean debunking, I may have disappointed you. The honest picture is messier than both.

Rituals are not magic. They are also not placebo in the dismissive sense of the word — placebo effects are real effects. They are psychological tools with genuine mechanisms: anxiety regulation, attention training, self-efficacy reinforcement, and behavioral commitment. These mechanisms can and do influence the decisions and behaviors that drive financial outcomes.

What they cannot do is bypass the requirement for actual financial action, actual financial literacy, or actual structural improvement to your income and expenses.

The most powerful function of a money ritual is not what it does to the universe — it is what it does to your avoidance. Financial anxiety is extraordinarily common, extraordinarily harmful, and extraordinarily under-addressed by financial advice that treats people as rational actors who simply need the right information. A daily ritual that reliably gets you to open your accounts, sit with your numbers, and make one intentional decision is worth more than any optimization strategy you could apply to an avoidance pattern you refuse to confront.

The trade-off you have to make honestly: a satisfying ritual that substitutes for action is worse than no ritual at all. If your morning practice feels good and leaves you feeling like you’ve already handled your money — without having touched your money — it has become part of the problem.

Primary Sources

- Wang, X. & Yin, K. (2025). “Psychological Approaches to Good Luck: The Role of Rituals in Uncertainty.” Social Psychological and Personality Science. View study

- Brooks, A.W. et al. (2016). “Don’t stop believing: Rituals improve performance by decreasing anxiety.” Organizational Behavior and Human Decision Processes, 137, 71–85. Harvard Business School. View study

- Damisch, L., Stoberock, B., & Mussweiler, T. (2010). “Keep Your Fingers Crossed!” Psychological Science, 21(7). View study

Secondary Sources

- Norton, M. (2024). The Ritual Effect. Harvard Business School Press. Author interview

- Hobson, N. et al. “The Psychology of Rituals: An Integrative Review.” University of California, Berkeley. View paper

- Klontz, B. Research on Money Scripts and Financial Psychology. Behavioral Finance overview

Related Articles

Last Updated: May 2025 · Neural Grimoire · neuralgrimoire.com